- Market Divergence: The global economy is caught between two opposing forces: inflationary energy disruptions in the Middle East (weighing on bond markets) and massive AI infrastructure spending (fueling equity market resilience).

- Unprecedented AI Investment: Technological “hyperscalers” are driving a historic capital expenditure cycle, projected to reach $1 trillion by 2027, which is currently offsetting the modest growth dampening caused by higher energy prices.

- Strategic Value and EM Exposure: Investors can access AI growth more affordably through “AI at a discount” themes, such as Emerging Markets—where technology now makes up nearly 40% of indices—and Value ETFs that benefit from semiconductor supply bottlenecks.

- Inflation Resilience: While energy shocks pressure central banks to consider rate hikes rather than cuts, value stocks serve as a critical portfolio hedge, as they historically outperform during periods of high and volatile inflation.

OUTLOOK

Markets and headlines often diverge, but today many market observers are perplexed by the ongoing gloomy headlines and the robustness of the stock market. Two opposing forces are at work: the disruption of energy supplies through the Strait of Hormuz, which is feeding through to global inflation and beginning to weigh on growth, versus the vast spending on AI, which is providing a powerful tailwind to economic growth and corporate earnings. The former is reflected in the bond market; the latter in the eye-catching performance of equity markets.

The ongoing energy disruption in the Middle East is an unwelcome reminder of the impact of higher energy prices in 2022 in the wake of the invasion of Ukraine. Those with longer memories or an interest in economic and market history look back at the 1970s to see what damage an energy crisis can wreak. On that count, it’s worth remembering that the global economy has evolved and grown significantly in the last fifty years, whilst dependence on oil as an energy source has fallen as clean energy has become a more significant portion of global energy supply, and major economies have become more service sector driven. However, the impact of rising energy prices is felt around the world with consumers feeling the effects of higher petrol and household electricity prices. This feeds into inflation and is forcing central banks to consider rate hikes rather than cuts, which was the expectation prior to the conflict. So, whilst stock markets have been resilient, bond markets around the world have been impacted by this about-turn by central bankers.

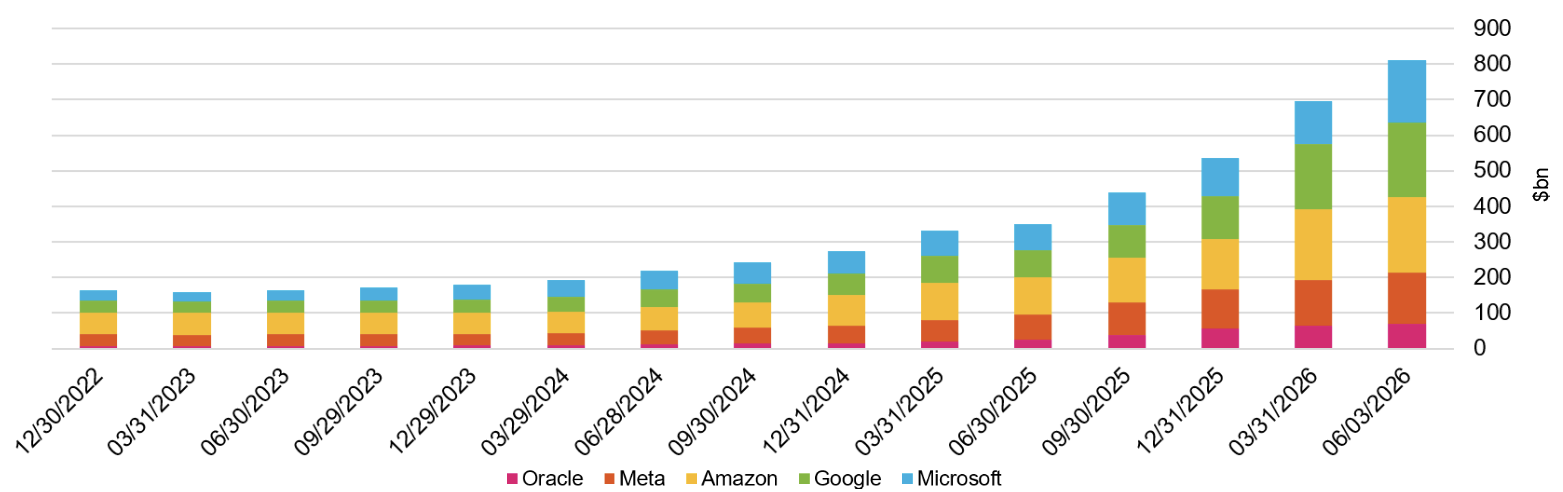

The equity market, on the other hand, seems oblivious to what the International Energy Agency described as “the largest supply disruption in the history of the global oil market”. Is it in denial? The reason for this is that the impact on growth has been modest and so far, more than offset by the boost in growth from AI spending. The scale and speed of capex spending by the hyperscalers – Amazon, Alphabet, Meta and Microsoft plus Oracle – is hard to conceptualise. Collectively they are forecast to spend an eye-watering $700 billion this year and over $1 trillion in 2027. This spending already far outweighs the investment in telecom fibre in the 1990s to support the explosive growth of the Internet. Whilst some of the largest telecom companies funded their expansion through debt and paid a heavy price once the internet bubble popped, the balance sheets of the Magnificent Seven started off pristine. How their balance sheets evolve over the next few years will be critical to the sustainability of this extraordinary capex cycle.

Hyperscaler CAPEX estimate for next 12 months

Our approach has been to engage with this theme, but to do so in a diversified manner, without doubling up on those US megacap technology names that dominate the index. Our “AI at a discount” theme includes investment trusts with exposure to public and private AI companies trading at large discounts to NAV, robotics, biotech and health tech, and clean energy stocks. These allocations are either direct or indirect beneficiaries of this extraordinary technology and in aggregate trade at a valuation discount to the market. Clean energy scores twice as a beneficiary of both the supply shock from the Middle East and the demand shock from AI infrastructure spending on data centres.

Perhaps the most surprising beneficiary of AI spending has been our exposure to semiconductor stocks through our Value ETFs both in the US and Emerging Markets. Emerging market indices have historically been considered cyclical and commodity linked, but quietly over the past 15 years the weight of technology stocks in these indices has crept up, from around 10% to nearly 40% today – particularly businesses based in Korea and Taiwan. Many investors have failed to notice that the technology weighting in Emerging Markets now exceeds that in the US, although moving Google and Amazon into Communications and Consumer Discretionary respectively, has certainly helped. We were drawn to these sector neutral Value ETFs due to their extreme valuation discount on multiple metrics, and today many of their technology holdings are key beneficiaries of the bottlenecks in both memory and semiconductor production, leading to soaring earnings. Stocks that are priced for lacklustre growth can deliver truly spectacular returns with an earnings tailwind. But we also know from experience that these supercycles don’t go on forever.

Value stocks have one more trick up their sleeve: they have historically outperformed as inflation picks up. Looking back over the last 100 years, value stocks have outperformed in most decades, with the underperformance in the 2010s being the exception, not the rule. In decades where inflation has run hot, value stocks have tended to outperform, with the 1970s being the most extreme example when inflation ran at over 7% per year and value stocks outperformed by a similar margin. We should all hope that we don’t have a repeat of that decade, which was a dismal period for investors, but in a world of higher and more volatile inflation, value stocks are an important part of the toolkit.

The relationship between inflation and value investing for each decade from the 1920’s to the 2010’s

CONCLUSION

Despite the considerable gloominess and the potential economic impact of the energy disruption caused by the Middle East, there are reasons to be hopeful. The capex spending of the hyperscalers is unprecedented and is leading to a pickup in both growth and earnings for downstream businesses. However, the impact of the disruption to energy supply through the Strait of Hormuz will start to bite from a growth perspective if it remains unresolved over the summer and so a balanced, diversified approach remains key.