Equities continued their upward trajectory with major equity indices posting gains; however, volatility remained elevated as markets navigated several challenges last month.

AI displacement concerns triggered a sell-off in software companies after AI developers like Anthropic announced the launch of AI tools with the potential to automate numerous professional services. The US Supreme Court ruled against the current administration’s use of IEEPA to enact tariffs, prompting the administration to impose blanket tariffs for 150 days under an alternative legal provision. Meanwhile, geopolitics once again took centre stage as US and Israeli forces launched strikes on Iran – a situation that continues to develop with potentially far-reaching consequences.

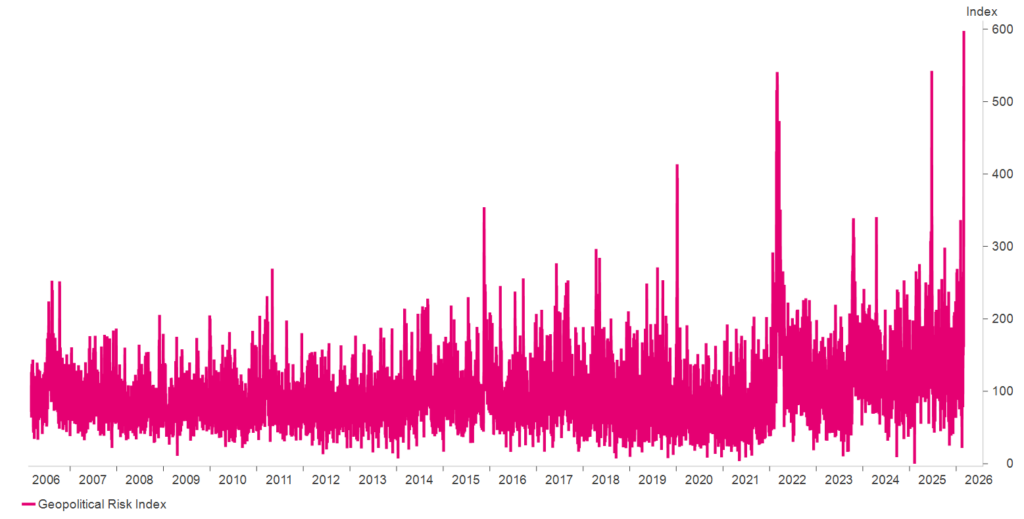

Coming into the year, we described geopolitical risk as a “known unknown.” We knew that geopolitics would be a risk factor; we simply did not know when it would materialise or the magnitude of its impact. Just two months into the year, geopolitical risk has already reached a 20-year high (see Figure 1).

Figure 1: Geopolitical Risk Index (Source: Macrobond, February 2026)

At the time of writing, markets have behaved broadly in line with historical patterns during past geopolitical risk events, with equities selling off, government bonds rallying, and commodities- specifically oil and gas – surging. Oil and gas rallied on news that Iranian officials closed the Strait of Hormuz, a narrow body of water connecting the Persian Gulf and the Gulf of Oman, which serves as a critical artery for global energy supply. Over 20% of the world’s oil and gas passes through this strait, and the situation was further compounded by the Rumaila oil field in Iraq halting production.

Research shows that equity market pullbacks resulting from geopolitical events are often short-lived, with markets typically recovering in the months following such events. However, we are cognisant that this escalation in geopolitical risk has emerged at a time when inflationary pressures had been moderating in the West. The longer this situation persists, the greater the risk of reigniting inflation as higher oil and gas prices transmit through the global economy.

For equity markets, this translated into continued regional performance dispersion, with US equities lagging as investors shunned richly valued technology companies and favoured asset-intensive sectors such as energy and utilities.

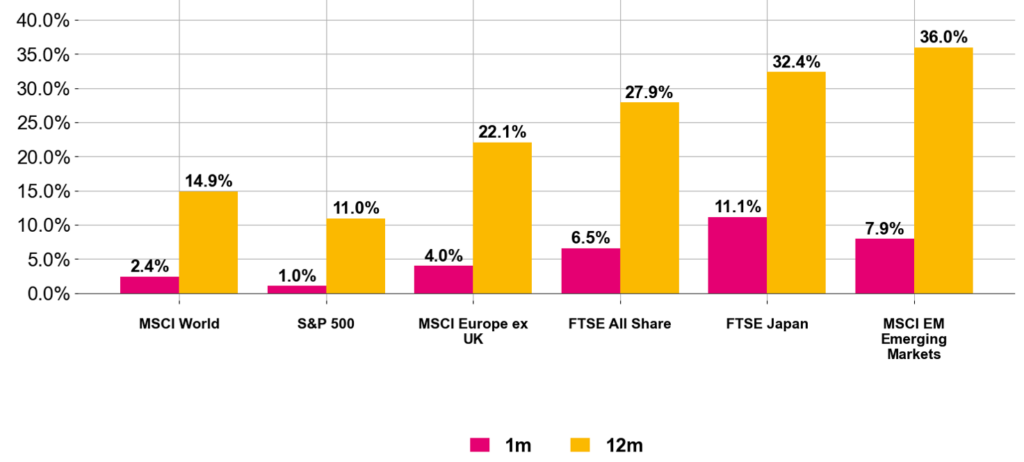

This benefited UK equities, which rose 6.5% last month, supported by the rotation away from AI stocks and rising energy prices. Emerging markets continued to benefit from the AI infrastructure build-out, with manufacturers in Asia and raw material providers in Latin America gaining as investors sought exposure to the beneficiaries of massive AI capital expenditure without the exorbitant valuations. Japanese equities, however, were the standout performer as Takaichi and the LDP secured a landslide victory on 8 February – the biggest victory for the LDP since its creation 70 years ago – which will enable further expansionary fiscal policy (see Figure 2).

Figure 2: Regional Equity returns (Source: Pacific Asset Management, February 2026)

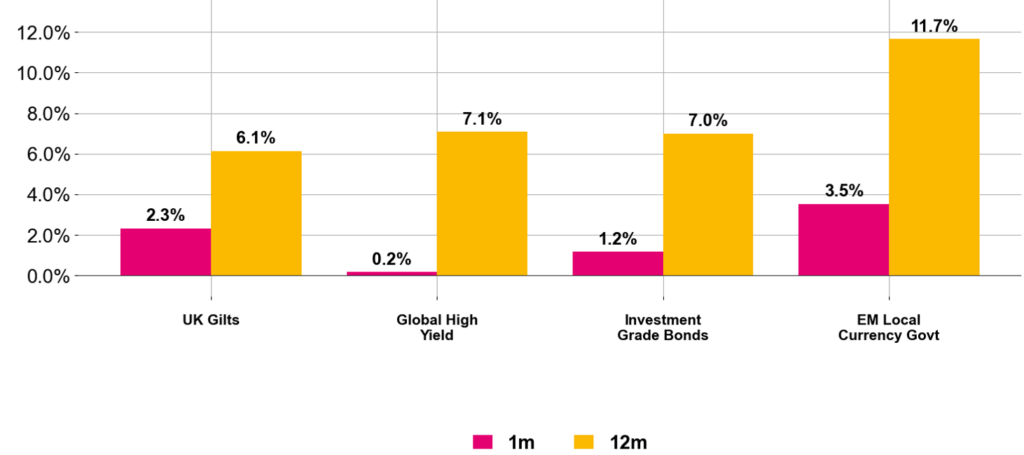

Within fixed income, government bonds rallied with yields falling across the US, UK, and Europe, reflecting increasing geopolitical risk, uncertainty, and a benign inflation backdrop. UK gilts led the way, returning over 2% following news that inflation fell to 3% in January – the lowest reading since March 2025 – alongside the announcement that UK government debt sales are expected to decline for the first time in four years. Meanwhile, there was little spillover from the private credit sector, despite the announcement that Blue Owl would halt redemptions within one of its private credit funds, as both investment grade and high yield bonds posted positive returns with higher quality names outperforming lower quality names.

Figure 3: Fixed Income returns (Source: Pacific Asset Management, February 2026)

Looking ahead, the contrast between the narrative – “the noise” – and fundamentals looks set to continue. Fundamentals remain robust; however, this escalation in geopolitical risk is a source of volatility, and the continued disruption from AI looks set to persist. Given this backdrop, investors are well placed to avoid constraining themselves geographically and to recognise that diversification during periods of stress can help not only reduce risk but also enhance returns.