- Despite heightened political and media volatility, global markets remain resilient near all-time highs, supported by strong corporate earnings and a favourable macro backdrop.

- The next phase of AI investment lies in “second-derivative” beneficiaries, particularly biotech and health technology, where valuations are historically low and AI is accelerating drug discovery, clinical data analysis, and surgical innovation.

- A “stealth bull market” in value stocks has emerged. Sector-neutral value strategies and cheaper stocks across regions have outperformed, while trading at deep discounts relative to broader indices.

- Gold’s role has expanded from an inflation hedge to protection against institutional and fiscal risks. Central bank demand and global debt pressures support the long-term case, though positions should be managed tactically.

OUTLOOK

Navigating the Conundrum: Headline Volatility vs. Market Resilience

Since the start of the Trump presidency, investors have been faced with a stark contrast between a volatile news cycle and resilient market performance. From threats to Federal Reserve independence amid a DOJ investigation, wild headlines regarding Greenland and Iran, the “wall of worry” has rarely been higher. And yet global markets remain near all-time highs. This resilience is driven by the same engine that fuelled the strong performance of 2025: corporate earnings remain robust, and the macro backdrop remains supportive of risk assets.

We believe the key for 2026 lies in diversifying away from the stretched valuations of parts of the S&P 500 and into three themes: AI at a discount, the stealth bull market in value stocks and the timeless diversifier of gold.

AI’s Second Act: Biotech and Health Technology

The AI “arms race” has entered a mature phase of massive capital expenditure, with hyperscalers now spending $500bn – $650 bn on data centres in 2026. While the market remains obsessed with the first-derivative winners, we are looking toward the “second derivative” – sectors where AI is being applied to solve massive data problems.

Chief among these is Biotech and Health Technology. While some investors feared headwinds from the new administration’s healthcare appointments, including Robert F Kennedy Jnr, the underlying reality is a push to accelerate U.S. biotech leadership. Biotech is currently trading at some of the lowest valuations we have ever seen relative to the S&P 500.

Patent cliffs are a problem for big pharma, with $200bn of branded drug sales rolling off patent over the next decade, which will then be open to generic drug replication.

Biotech is integral to the drug discovery process, with these companies accounting for 70% of new drug approvals in 2024, up from just 26% from a decade ago. And AI is already transforming this sector by organising clinical data and speeding up the decade long R&D process by approximately one year. In a world of 20-year patents, saving a year in development and thereby adding 10% to the high-margin sales life of a drug is a massive value driver. We are also seeing AI increasingly used in Health Technology, where systems like the DaVinci 5 robotic surgery platform utilise 10,000 times the compute power of previous models to provide real-time feedback to surgeons.

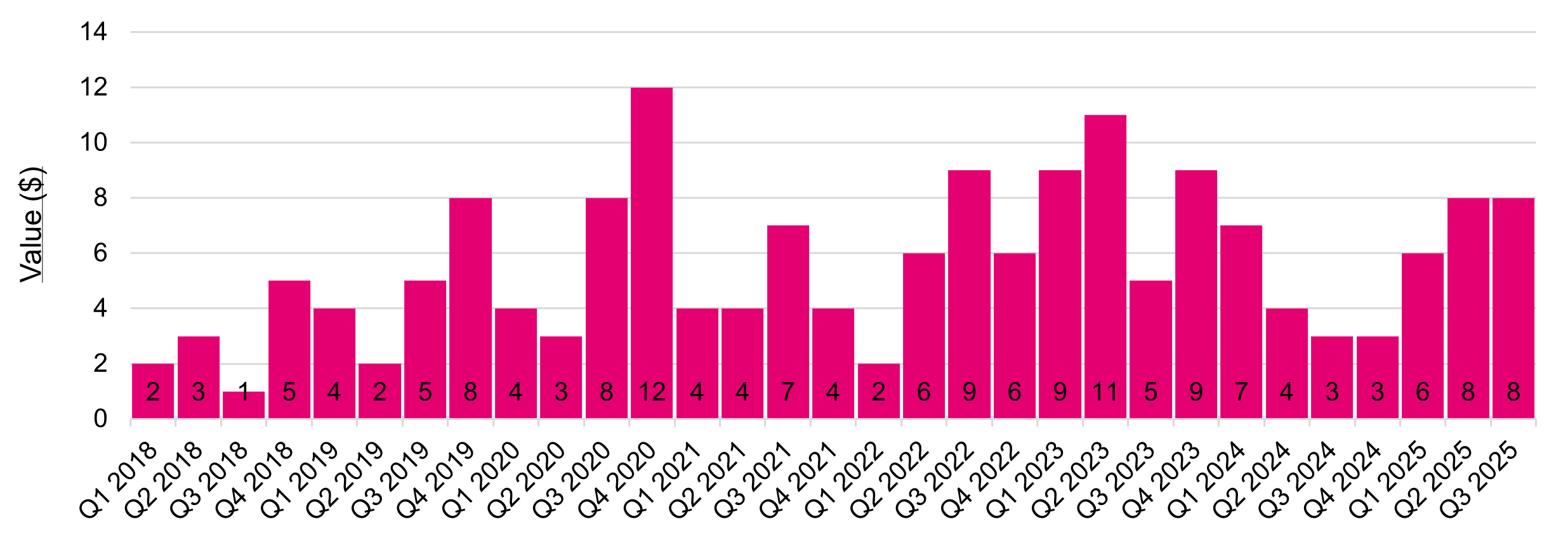

Finally, M&A activity is picking up, with the CEO of Novo Nordisk commenting in January that “As long as it’s complementary to our own assets, then we can go very big in buying something in,” we see a pickup in announced public biotech M&A transactions.

Announced Public Biotech M&A Transactions – number and $ value

The Stealth Bull Market in Value

While the “Magnificent Seven” dominated the headlines, 2025 saw a “stealth bull market” in Value stocks that few have noticed. The “Value 2.0” approach we utilise is sector-neutral; we don’t bet on one industry but rather own the cheapest stocks within every sector at the weights of the market.

The results from this approach have been quietly impressive. Last year, the cheapest stocks in the technology sector outperformed the broader S&P 500 by nearly 30% for example. And in fact, 8 of the 11 sectors in the S&P outperformed in 2025. Despite this, the valuation gap between market cap and sector neutral value remains staggering: the S&P 500 trades at over 22x forward earnings, while our value basket trades at just 7.5x – a 70% discount. The same story can be seen in other regions. In Europe, all value sectors outperformed their market cap equivalent, whilst still trading on a 30% discount, and in emerging markets the story is similar, 8 sectors outperformed, the discount remains at 40% and yet these stocks were up more than 30% for the year.

In the U.S., a company like Micron trades at a fraction of the multiples of its high-flying peers despite benefiting from the same AI demand via leadership in memory (DRAM). In Emerging Markets, “sleepy” companies like Hyundai are being re-rated as they reveal themselves to be high-tech leaders in robotics (via ownership of Boston Dynamics).

We believe paying 8x earnings for these “Value” champions provides a natural margin of safety that some market-cap-weighted indices currently lack.

Performance of Value (US, Europe, EM) and MSCI World

Gold: The Timeless Diversifier

Finally, the case for gold has evolved from a simple inflation hedge to a critical diversifier against institutional volatility. Attacks on the independence of the Federal Reserve and the politicisation of the dollar have led global central banks to double their gold allocations-from an average of 14% to 28% in recent years.

Furthermore, the issue of “fiscal excess” remains a huge problem for governments around the world and a tailwind for gold. Global governments are now spending roughly $5 trillion annually just to service their debt. In an environment of persistent deficits and a weakening dollar, gold is the ultimate beneficiary.

We prefer to express this view through a combination of both physical gold and gold miners, who are currently exhibiting rare capital discipline. More recently, gold and miners have come under pressure due to crowded positioning and some commentators suggesting that Trump’s nominee to be Fed chair may be more hawkish than anticipated. Our view is that whilst Gold remains important to portfolios, it is also vital to be able to trade these positions tactically, as markets appear to be moving faster than ever, as such we did reduce our Gold prior to the sell-off due to its extreme strength, giving us optionality to add back to the position.

CONCLUSION

While we expect more volatility as we head toward the November midterms, we remain positive on equities. However, success in 2026 will not come from simply “buying the index.” By rotating into undervalued AI beneficiaries in healthcare, capturing the stealth bull market in value, and maintaining a disciplined position in gold, we believe portfolios can remain resilient regardless of the headlines. Diversification remains our most valuable tool in an uncertain world.